5 Main Ingredients of a Credit Score

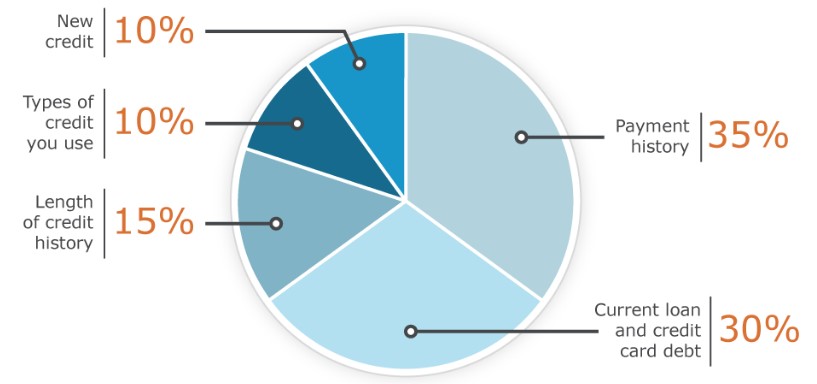

Credit Scores take into consideration five main categories of information in a credit report. The chart below shows the relative importance of each category to Credit Scores.

A Sample Pie chart describing the Credit Score ingredients, including 35% payment history, 30% current loan and credit card debt, 15% length of credit history, 10% types of credit you use, and 10% new credit.

Below is a detailed breakdown of each category. As you review this information, keep in mind that:

- Credit Scores take into consideration all of these categories, not just one or two.

- The importance of any factor (piece of information) depends on the information in your entire credit report.

- Credit Scores look only at the credit-related information on your credit report.

- Credit Scores consider both positive and negative information on your credit report.

Payment History

Approximately 35% of a Credit Score is based on this information, which includes:

- Payment information on many types of accounts:

- Credit cards – such as Visa, MasterCard, American Express and Discover.

- Retail accounts – credit from stores where you do business, such as department store credit cards.

- Installment loans – loans where you make regular payment amounts, such as car loans and mortgage loans.

- Finance company accounts.

- Public record and collection items – reports of events such as bankruptcies, foreclosures, lawsuits, wage attachments, liens and judgments.

- Details on late or missed payments (“delinquencies”) and public record and collection items.

- The number of accounts that show no late payments or are currently paid as agreed.

Credit Utilization Ratio (Current loan and credit card debt)

Approximately 30% of a Credit Score is based on information which evaluates your indebtedness. In this category, Credit Scores take into account:

- The amount owed on all accounts.

- The amount owed on different types of accounts.

- Whether you are showing a balance on certain types of accounts.

- The number of accounts where you carry a balance.

- How much of the total credit line is being used on credit cards and other revolving credit accounts.

- How much is still owed on installment loan accounts, compared with the original loan amounts.

Credit utilization, one of the most important factors evaluated in this category, considers the amount you owe compared to how much credit you have available. For example, if you have a $2,000 balance on one card and a $3,000 balance on another, and each card has a $5,000 limit, your credit utilization rate would be 50%. While lenders determine how much credit they are willing to provide, you control how much you use. Credit’s research shows that people using a high percentage of their available credit limits are more likely to have trouble making some payments now or in the near future, compared to people using a lower level of credit.

Having credit accounts with an outstanding balance does not necessarily mean you are a high-risk borrower with a low Credit Score. A long history of demonstrating consistent payments on credit accounts is a good way to show lenders you can responsibly manage additional credit.

Length of Credit History

Approximately 15% of a Credit Score is based on this information.

In general, a longer credit history will increase a Credit Score, all else being equal. However, even people who have not been using credit long can get a good Credit Score, depending on what their credit report says about their payment history and amounts owed. Regarding length of history, a Credit Score takes into account:

- How long your credit accounts have been established. A Credit Score can consider the age of your oldest account, the age of your newest account and the average age of all your accounts.

- How long specific credit accounts have been established.

- How long it has been since you used certain accounts.

New Credit

Approximately 10% of a Credit Score is based on this information.

Credit’s research shows that opening several credit accounts in a short period of time represents greater risk – especially for people who do not have a long credit history. In this category a Credit Score takes into account:

- How many new accounts you have opened

- How long it has been since you opened a new account.

- How many recent requests for credit you have made, as indicated by inquiries to the credit bureaus.

- Length of time since credit report inquiries were made by lenders.

- Whether you have a good recent credit history, following any past payment problems.

Looking for an auto, mortgage or student loan may cause multiple lenders to request your credit report, even though you are only looking for one loan. In general, Credit Scores compensate for this shopping behavior in the following ways:

- Credit Scores ignore auto, mortgage, and student loan inquiries made in the 30 days prior to scoring. So, if you find a loan within 30 days, the inquiries won’t affect your score while you’re rate shopping.

- After 30 days, Credit Scores typically count inquiries of the same type (i.e., auto, mortgage or student loan) that fall within a typical shopping period as just one inquiry when determining your score.

Types of Credit in Use

Approximately 10% of a Credit Score is based on this information.

Credit Scores consider your mix of credit cards, retail accounts, installment loans, finance company accounts and mortgage loans. It is not necessary to have one of each, and it is not a good idea to open a credit account you don’t intend to use. In this category a Credit Score takes into account:

- What kinds of credit accounts you have. Do you have experience with both revolving (credit cards) and installment (fixed loan amount and payment) accounts, or has your credit experience been limited to only one type?

- How many accounts you have of each type. A Credit Score also looks at the total number of accounts you have. For different credit profiles, how many is too many will vary depending on your overall credit picture.

This is for educational purposes only. Credit issuers have their own criteria for making credit decisions. There are many different Credit Score versions and other information when you apply for credit. There are many factors that a lender or credit provider looks at to determine your credit options; therefore, a specific Credit Score does not necessarily guarantee a specific loan rate, approval of a loan, or an automatic upgrade on a credit account. I do not provide credit repair services nor advice or assistance with rebuilding or improving your credit record, credit history, or credit rating.

Contact me for information and tips on how to improve your credit score

Jennifer Harper, Realtor | Executive Realty Services | Lic# S.0168752

Email: LasVegasHomesByJennifer@yahoo.com

Web: LasVegasHomesByJennifer.com

*************************************************

For a Free List of Homes For Sale click: Free list of Homes For Sale